The Logistic Model

GLM Models for Binary Variables

\(\newcommand{\VS}{\quad \mathrm{VS} \quad}\) \(\newcommand{\and}{\quad \mathrm{and} \quad}\) \(\newcommand{\E}{\mathbb E}\) \(\newcommand{\P}{\mathbb P}\) \(\newcommand{\Var}{\mathbb V}\) \(\newcommand{\Cov}{\mathrm{Cov}}\) \(\newcommand{\1}{\mathbf 1}\)

Context

\(Y\) is a binary variable \(Y_k \in \{0,1\}\)

\(X = (X^{(1)}, \ldots, X^{(p)})\) are \(p\) regressors

\(Y|X = x\) follows a Bernoulli distribution with parameter \(p(x) = P(Y = 1|X = x)\). Model:

\[p(x) = g^{-1}(x^T\beta)\]

where \(g^{-1}\) is a strictly increasing function with values in \([0, 1]\)

Approach: We begin by discussing the choice of \(g^{-1}\) (or \(g\))

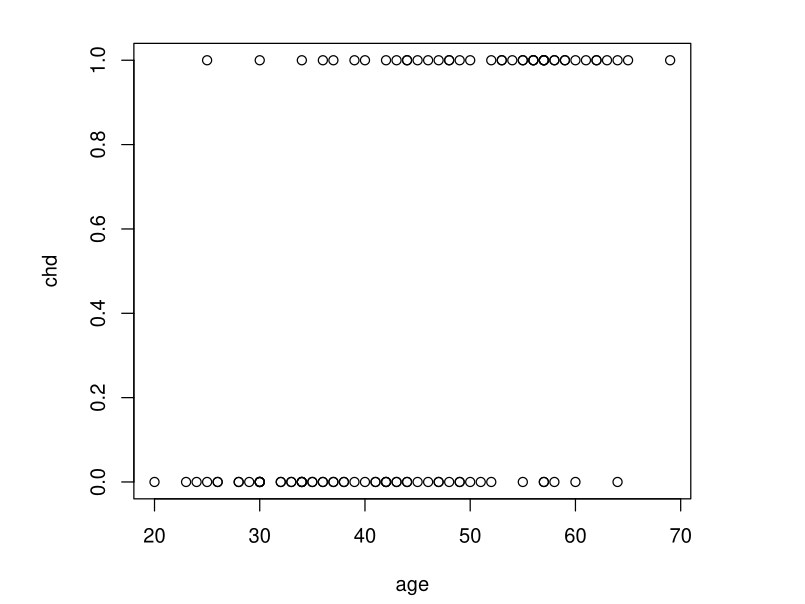

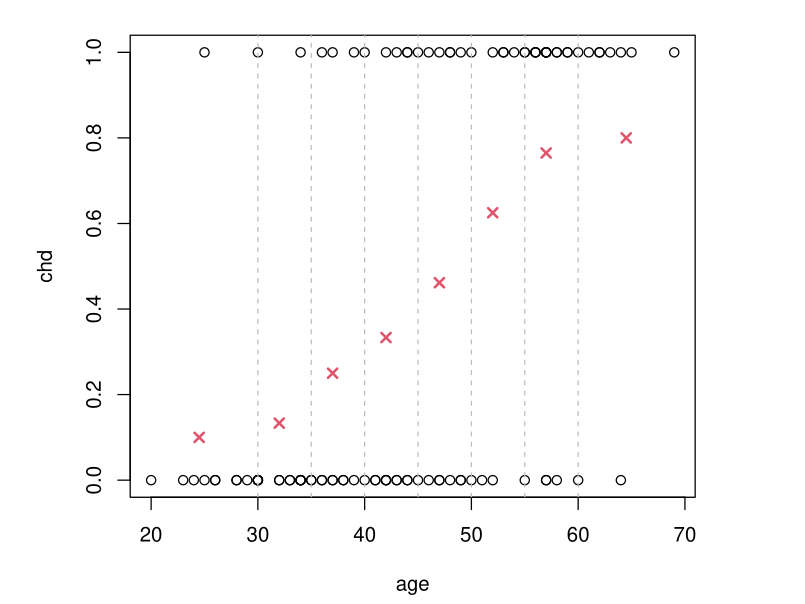

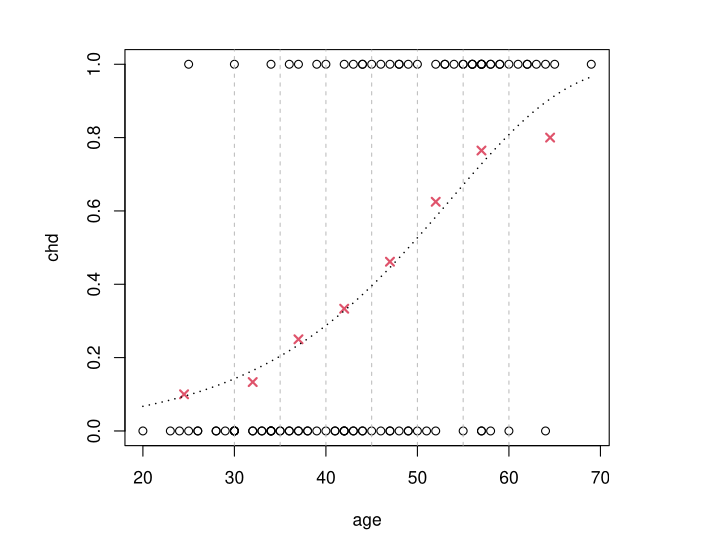

Example: Coronary Heart Disease

Data Description: Presence of chd as a function of age \(Y = \text{chd} \in \{0,1\}\), \(X = \text{age}\)

We want to estimate \(p(x) = \E(Y|X = x) = \P(\text{chd} = 1|X = x)\) for all \(x\)

Example: Simple Idea

- Group the \(x\) values by age class

- Calculate the proportion of \(chd = 1\) in the class containing \(x\)

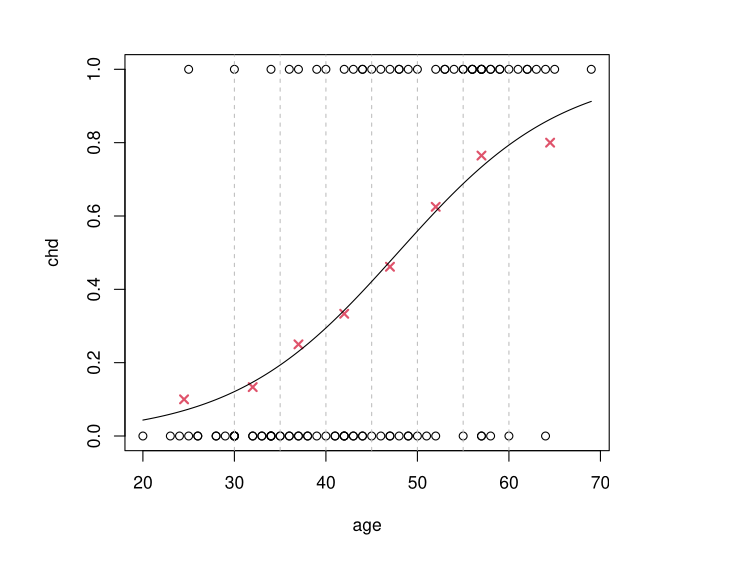

Example: GLM Approach

Objective: We want to model \(p(x) = P(\text{chd} = 1|X = x)\) by: \[p(x) = g^{-1}(\beta_0 + \beta_1 x)\]

Constraint: We need \(g^{-1}\) to have values in \([0, 1]\)

Example: The Logit Model

\[g^{-1}(t) = \frac{e^t}{1 + e^t} \quad \text{i.e.} \quad g(t) = \ln\left(\frac{t}{1-t}\right) = \text{logit}(t)\]

Results of \(g^{-1}(\hat \beta_0 + \hat \beta_1 x)\) obtained by MLE

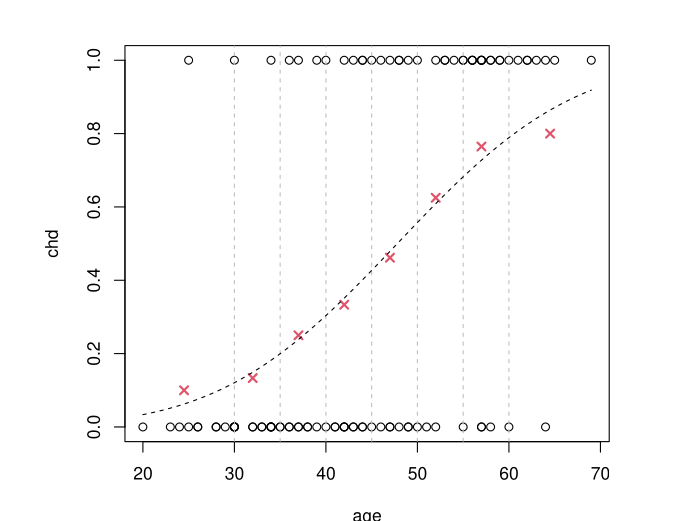

Example: The Probit Model

If \(\Phi\) is the CDF of a \(\mathcal{N}(0, 1)\) distribution, we take \(g^{-1}(t) = \Phi(t)\)

Results of \(g^{-1}(\hat \beta_0 + \hat \beta_1 x)\) obtained by MLE

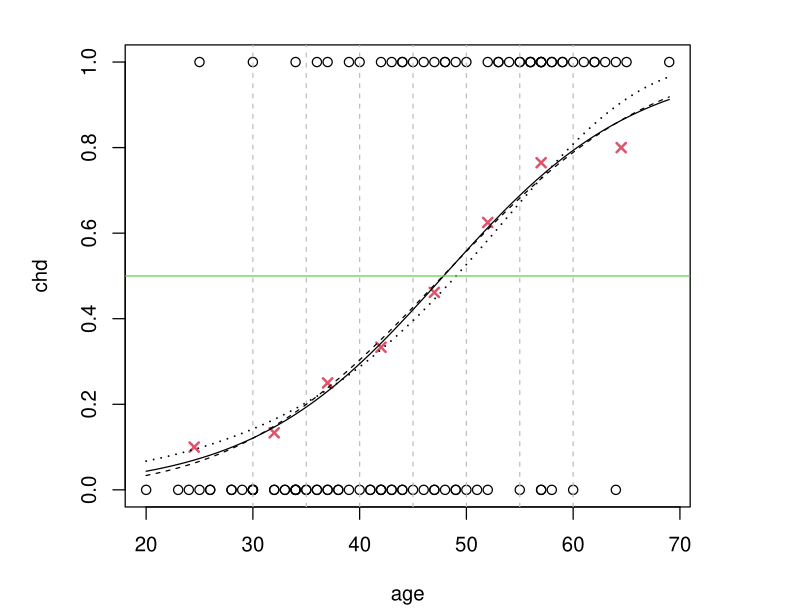

Example: Model cloglog

\[g^{-1}(t) = 1 - e^{-e^t}\]

Results of \(g^{-1}(\hat \beta_0 + \hat \beta_1 x)\) obtained by MLE

Example: Comparison of the Three Models

logit and probit give approximately the same result cloglog differs slightly and is not “symmetric”

Which Link Function to Choose for Binary Case?

Question: Which link function to choose in practice when \(Y\) is binary?

Default choice: By default, we favor the logit model

Exceptions: Unless there is a good reason to choose something else (probit model, complementary log-log, or log-log)

Next steps: We return to the 3 usual choices to justify this preference

Details on the Probit Model

The probit model is justified when the binary variable \(Y|X = x\) comes from thresholding a Gaussian latent variable \(Z(x)\):

\[(Y|X = x) = \mathbf{1}_{Z(x) \geq \tau}\]

where \(Z(x) \sim \mathcal{N}(x^T\beta, \sigma^2)\)

If \(\Phi\) is the CDF of a \(\mathcal N(0,1)\) \[P(Y = 1|X = x) = P(Z(x) \geq \tau) = \Phi\left(\frac{x^T\beta - \tau}{\sigma}\right)\]

Examples in Probit Model

- \(Y\) represents a purchase decision, and \(Z(x)\) quantifies the utility of the good

- \(Y\) is a declared psychological state (happiness, depression) and \(Z(x)\) is a latent, unobserved measure of personal satisfaction

Probit vs Logit: Current Trends

Econometricians: The probit model remains relatively popular among econometricians…

General trend: but it tends to be replaced by the logistic model

Advantages of logit: The logit model has many advantages that probit does not have:

- Interpretation of results

- Explicit formulas

Theoretical justification: CDF of probit close to CDF of logit

Remarks on cloglog Model

The modeling approach is \(p(x) = g^{-1}(x^T\beta)\) with

\[g(t) = \ln(-\ln(1-t)) \quad \text{i.e.} \quad g^{-1}(t) = 1 - e^{-e^t}\]

Not symmetric in the sense that \(g(t) \neq -g(1-t)\).

\(p(x)\) approaches \(0\) slowly but \(1\) very rapidly

If the opposite is true: take \(g(t) = -\ln(-\ln(t))\) (loglog model)

Useful in survival models (e.g. Cox)

Details on the Logit Model

Highly valued interpretation tool: odds-ratios.

More “practical” from a theoretical point of view.

Natural model in many situations.

Theoretical Motivation of Logit

We will show in exercises that:

If the two groups of individuals associated with \(Y = 0\) and \(Y = 1\) have a Gaussian distribution of \(X\) with different means, i.e. for \(m_0 \neq m_1\),

\(X|(Y = 0) \sim \mathcal N(m_0, \Sigma) \and X|(Y = 1) \sim \mathcal N(m_1, \Sigma)\)

then \(\mathbb P(Y = 1|X = x)\) follows a logistic model.

The previous result remains true for any distribution from the exponential family instead of \(\mathcal N\).

Summary for Binary Variables

If \(Y\) is a binary variable, \((Y|X = x) \sim \mathcal B(p(x))\).

In a GLM model for \(Y\), we set \(p(x) = g^{-1}(x^T\beta)\) where \(g\) is:

by default the logit function, which is the most natural;

possibly probit if we have good reasons to justify it (but the results will be similar to logit);

cloglog (or loglog) if we have good reasons to justify it (strong asymmetry of \(p(x)\), connection with a Cox model).

In the following, we will focus on the logit model.

Outline

- interpret the model,

- estimate \(\beta\) from a dataset,

- evaluate the quality of estimation,

- exploit it to make predictions/classification.

Model Interpretation

Interpretation of the Logistic Model

If \(x=(x^{(1)}, \dots, x^{(p)}) \in \mathbb R^{p \times 1}\)

\[p(x) = \text{logit}^{-1}(x^T\beta) = \frac{e^{x^T\beta}}{1 + e^{x^T\beta}}\]

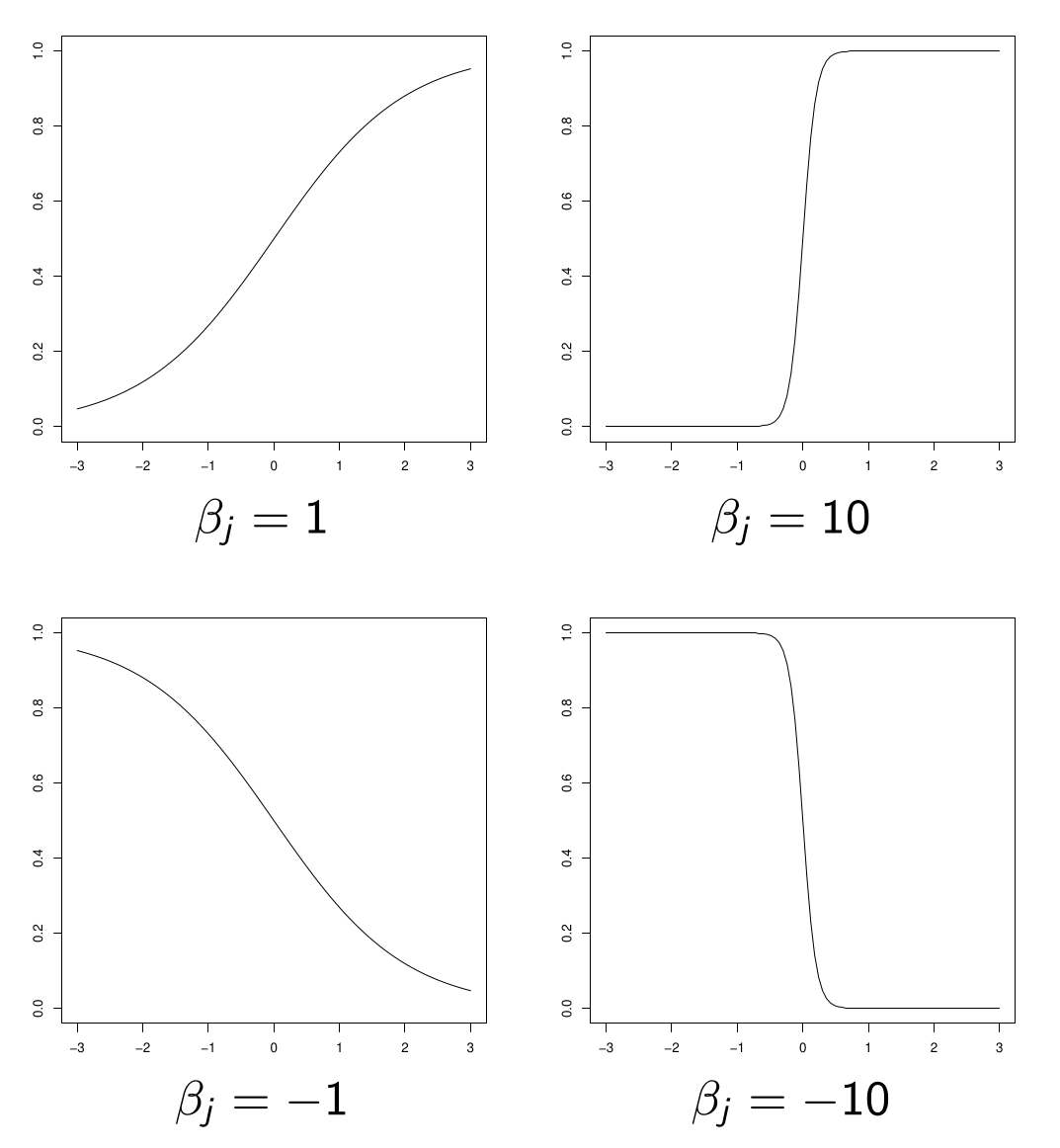

\(x^{(j)} \to p(x)\) is increasing if \(\beta_j > 0\), decreasing otherwise.

The larger \(|\beta_j|\) is, the stronger the discriminatory power of regressor \(X^{(j)}\) (a small variation in \(x^{(j)}\) can cause a large variation in \(p(x)\)).

Shape of logit function

shape of \(x^{(j)} \to p(x)\)

Example: BMI Study (French: IMC)

For each of the 5300 patients, we observe:

- \(Y\): 1 if BMI > 35, 0 otherwise

- AGE

- DBP: low pressure (diastolic)

- SEXE: male or female

- ACTIV: 1 if intense sports activity, 0 otherwise

- WALK: 1 if walking or cycling to work, 0 otherwise

- MARITAL: marital status (6 categories: married, widowed, divorced, separated, single or cohabiting)

Model Definition

We seek to model \(P(Y = 1|X)\) where \(X\) groups the previous variables (excluding \(Y\)).

Model Results

| Variable | Estimate | Std. Error | z value | Pr(> | z |

|---|---|---|---|---|---|

| (Intercept) | -2.810240 | 0.294316 | -9.548 | < 2e-16 | *** |

| AGE | -0.004407 | 0.002717 | -1.622 | 0.105 | |

| DBP | 0.017581 | 0.003283 | 5.356 | 8.53e-08 | *** |

| SEXEFEMME | 0.544916 | 0.081261 | 6.706 | 2.00e-11 | *** |

| WALK1 | -0.409344 | 0.095972 | -4.265 | 2.00e-05 | *** |

| ACTIV1 | -0.789734 | 0.126653 | -6.235 | 4.51e-10 | *** |

| MARITAL2 | 0.070132 | 0.149638 | 0.469 | 0.639 | |

| MARITAL3 | -0.071318 | 0.127510 | -0.559 | 0.576 | |

| MARITAL4 | 0.188228 | 0.206598 | 0.911 | 0.362 | |

| MARITAL5 | 0.070613 | 0.115928 | 0.609 | 0.542 | |

| MARITAL6 | -0.150165 | 0.157687 | -0.952 | 0.341 |

The interpretation is similar to that of a linear regression model.

We want to remove the MARITAL variable from the model.

Model Results with AGE²

| Variable | Estimate | Std. Error | z value | Pr(> | z |

|---|---|---|---|---|---|

| (Intercept) | -3.9564361 | 0.3155529 | -12.538 | < 2e-16 | *** |

| AGE | 0.0640837 | 0.0123960 | 5.170 | 2.34e-07 | *** |

| I(AGE^2) | -0.0006758 | 0.0001260 | -5.364 | 8.14e-08 | *** |

| DBP | 0.0121546 | 0.0033775 | 3.599 | 0.00032 | *** |

| SEXEFEMME | 0.5155651 | 0.0776229 | 6.642 | 3.10e-11 | *** |

| WALK1 | -0.4042257 | 0.0913195 | -4.426 | 9.58e-06 | *** |

| ACTIV1 | -0.6573558 | 0.1150226 | -5.715 | 1.10e-08 | *** |

For someone for which WALK1=0 and ACTIV1=0:

\(P(Y = 1|\text{AGE}, \text{DBP}) = \text{logit}^{-1}(-3.95 + 0.064 \times \text{AGE} - 0.00068 \times \text{AGE}^2 + 0.0122 \times \text{DBP})\)

For someone for which WALK1=0 and ACTIV1=1:

\(P(Y = 1|\text{AGE}, \text{DBP}) = \text{logit}^{-1}(-3.95 + 0.064 \times \text{AGE} - 0.00068 \times \text{AGE}^2 + 0.0122 \times \text{DBP} \color{red}{ - 0.657})\)

Odds

\[\text{odds} = \frac{p}{1-p}\]

Betting interpretation for example, \(3\) to \(1\) means that for \(3\) people betting on \(A\), \(1\) person bets on \(B\).

So a randomly chosen bettor has a probability of \(p=3/4\) of betting on \(A\) and \(1-p=1/4\) on betting on \(B\)

Odds given X=x

Similarly, the odds of obtaining \(Y = 1\) given \(X = x\) is:

\[\text{odds}(x) = \frac{p(x)}{1 - p(x)}\]

where \(p(x) = P(Y = 1|X = x)\).

Odds Ratio

If two individuals have characteristics \(x_1\) and \(x_2\) respectively, we call the odds ratio between \(x_1\) and \(x_2\):

\[OR(x_1, x_2) = \frac{\text{odds}(x_1)}{\text{odds}(x_2)} = \frac{\frac{p(x_1)}{1-p(x_1)}}{\frac{p(x_2)}{1-p(x_2)}}\]

Warning

DO NOT CONFUSE ODDS RATIO WITH PROBABILITY RATIO

Only possible exception: if \(p(x_1)\) and \(p(x_2)\) are very small because then \(1 - p(x_1) \approx 1\) and \(1 - p(x_2) \approx 1\), so that \(OR(x_1, x_2) \approx p(x_1)/p(x_2)\)

Link with Proba. Ratio

However, it remains that:

\[\begin{aligned} OR(x_1, x_2) > 1 &\Leftrightarrow \frac{p(x_1)}{p(x_2)} > 1\\ OR(x_1, x_2) < 1 &\Leftrightarrow \frac{p(x_1)}{p(x_2)} < 1\\ OR(x_1, x_2) = 1 &\Leftrightarrow \frac{p(x_1)}{p(x_2)} = 1 \end{aligned}\]

Other Property of Odds Ratio

\(OR(x_1, x_2)\) accentuates the differences compared to \(p(x_1)/p(x_2)\):

\[\begin{aligned} OR(x_1, x_2) > \frac{p(x_1)}{p(x_2)} &\text{ when } OR(x_1, x_2) > 1\\ OR(x_1, x_2) < \frac{p(x_1)}{p(x_2)} &\text{ when } OR(x_1, x_2) < 1 \end{aligned}\]

Examples Using Odds Ratios

A logistic regression is most often used to compare the behavior of two individuals with respect to the variable of interest.

Examples:

- probability of purchase depending on whether or not one has been the subject of a personalized promotion;

- for a given vehicle, probability of experiencing a breakdown according to age;

- probability of recovery according to the treatment used;

Odds Ratio in Logistic Regression

It holds that \(\text{odds}(x) = \frac{p(x)}{1 - p(x)} = \exp(x^T \beta)\)

Hence,

\(OR(x_1, x_2) = \frac{\text{odds}(x_1)}{\text{odds}(x_2)} = \exp((x_1 - x_2)^T \beta)\)

If the two individuals differ only by regressor \(j\), then

\(OR(x_1, x_2) = \exp(\beta_j (x_1^{(j)} - x_2^{(j)}))\)

If regressor \(j\) is binary (\(x_1^{(j)} = 1\) while \(x_2^{(j)} = 0\)):

\(OR(x_1, x_2) = \exp(\beta_j)\)

Key Summary Statement

In a logistic regression model, \(\beta_j\) is interpreted as the logarithm of the odds-ratio between two individuals differing by a quantity of \(1\) on regressor \(j\), all else being equal.

In brief: \(\exp(\beta_j) = OR(x^{(j)} + 1, x^{(j)})\)

If regressor \(j\) is binary (absence or presence of a certain characteristic):

\(\exp(\beta_j)\) is simply the OR between the presence or absence of this characteristic, all else being equal.

Example 1: Intense Sports Activity

| Variable | Estimate | Std. Error | z value | Pr(> | z |

|---|---|---|---|---|---|

| (Intercept) | -3.9564361 | 0.3155529 | -12.538 | < 2e-16 | *** |

| AGE | 0.0640837 | 0.0123960 | 5.170 | 2.34e-07 | *** |

| I(AGE^2) | -0.0006758 | 0.0001260 | -5.364 | 8.14e-08 | *** |

| DBP | 0.0121546 | 0.0033775 | 3.599 | 0.00032 | *** |

| SEXEFEMME | 0.5155651 | 0.0776229 | 6.642 | 3.10e-11 | *** |

| WALK1 | -0.4042257 | 0.0913195 | -4.426 | 9.58e-06 | *** |

| ACTIV1 | -0.6573558 | 0.1150226 | -5.715 | 1.10e-08 | *** |

The Odds Ratio corresponding to practicing or not practicing intense sports activity is, all else being equal:

\(\exp(-0.657) \approx 0.52\)

The odds of obesity occurrence therefore decrease by half for individuals practicing intense sports activity.

(The odds, not the probability!)

Example 2: Diastolic Pressure

| Variable | Estimate | Std. Error | z value | Pr(> | z |

|---|---|---|---|---|---|

| (Intercept) | -3.9564361 | 0.3155529 | -12.538 | < 2e-16 | *** |

| AGE | 0.0640837 | 0.0123960 | 5.170 | 2.34e-07 | *** |

| I(AGE^2) | -0.0006758 | 0.0001260 | -5.364 | 8.14e-08 | *** |

| DBP | 0.0121546 | 0.0033775 | 3.599 | 0.00032 | *** |

| SEXEFEMME | 0.5155651 | 0.0776229 | 6.642 | 3.10e-11 | *** |

| WALK1 | -0.4042257 | 0.0913195 | -4.426 | 9.58e-06 | *** |

| ACTIV1 | -0.6573558 | 0.1150226 | -5.715 | 1.10e-08 | *** |

The OR for a diastolic pressure difference of \(+20\) is:

\(\exp(0.0121546 \times 20) \approx 1.28\)

The odds of obesity occurrence therefore increase by \(28\%\).

Estimation of the Parameters

The Framework

We observe \(n\) i.i.d. realizations \((Y_i, X_i)\) where \(Y_i \in \{0, 1\}\) and \(X_i \in \mathbb{R}^p\).

We denote \(p(x_i) = P(Y_i = 1|X_i = x_i)\).

The Logistic Model

We assume the logistic model: for all \(i\),

\[p(x_i) = \text{logit}^{-1}(x_i^T \beta) = \frac{e^{x_i^T \beta}}{1 + e^{x_i^T \beta}}\]

where \(\beta = (\beta_1, \ldots, \beta_p)^T\) and \(x_i^T \beta = \beta_1 x_i^{(1)} + \cdots + \beta_p x_i^{(p)}\).

Parameter Estimation

\[p(x_i) = \text{logit}^{-1}(x_i^T \beta) = \frac{e^{x_i^T \beta}}{1 + e^{x_i^T \beta}}\]

We will estimate \(\beta\) by maximizing the likelihood.

We will denote \(p_\beta(x_i)\) to emphasize the dependence of \(p(x_i)\) on \(\beta\).

Likelihood Calculation

For all \(i\), \(Y_i|(X_i = x_i)\) follows the distribution \(B(p_\beta(x_i))\). Therefore

\[P(Y_i = y_i|X_i = x_i) = p_\beta(x_i)^{y_i}(1 - p_\beta(x_i))^{1-y_i}\]

for all \(y_i \in \{0, 1\}\).

Likelihood

By independence, we obtain the likelihood

\[\ell(\beta, y_1, \ldots, y_n, x_1, \ldots, x_n) = \prod_{i=1}^n p_\beta(x_i)^{y_i}(1 - p_\beta(x_i))^{1-y_i}\]

Log-Likelihood

Taking the log and replacing \(p(x_i)\) by its expression, we obtain the log-likelihood:

\[\begin{aligned} L(\beta, y_1, \ldots, y_n, x_1, \ldots, x_n) &= \ln(\ell) \\ &=\sum_{i=1}^n \left[y_i x_i^T \beta - \ln(1 + e^{x_i^T \beta})\right] \end{aligned}\]

MLE Calculation

The MLE \(\hat{\beta}\), if it exists, cancels the gradient of \(L\) with respect to \(\beta\). This gradient equals

\[\frac{\partial L}{\partial \beta} = \sum_{i=1}^n x_i \left(y_i - \frac{e^{x_i^T \beta}}{1 + e^{x_i^T \beta}}\right)\]

We therefore need to solve a system of \(p\) equations with \(p\) unknowns.

But the solution is not explicit: we resort to numerical methods (Newton-Raphson algorithm)

Remarks on Optimization

This is a classic situation when using advanced statistical models: we often resort to optimization algorithms.

Does the solution exist? Is it unique?

MLE Uniqueness

Let \(X\) be the design matrix \((X^{(1)}, \dots, X^{(p)}) \in \mathbb R^{n \times p}\)

Proposition

If \(\text{rank}(X) = p\), then the MLE, if it exists, is unique.

Proof of MLE Uniqueness

It suffices to show that \(L\) is strictly concave in \(\beta\).

Hessian Matrix of \(L\):

\[\frac{\partial^2 L}{\partial \beta^2} = -\sum_{i=1}^n p_\beta(x_i)(1 - p_\beta(x_i)) x_i x_i^T\]

Hessian Properties

It is negative semi-definite. Moreover, for all \(u \in \mathbb{R}^p\),

\[\begin{aligned} u^T \frac{\partial^2 L}{\partial \beta^2} u = 0 &\Leftrightarrow u^T x_i x_i^T u = 0 \text{ for all } i\\ &\Leftrightarrow u^T x_i = 0 \text{ for all } i\\ &\Leftrightarrow Xu = 0\\ &\Leftrightarrow u = 0 \end{aligned}\]

since \(\text{rank}(X) = p\).

Conclusion

Thus, for all \(u \neq 0\),

\[u^T \frac{\partial^2 L}{\partial \beta^2} u < 0\]

The Hessian matrix is negative definite and therefore \(L\) is strictly concave,

The MLE is unique

About MLE Existence

Although \(L\) is strictly concave, its maximum can occur at infinity (think of the \(\ln\) function), in which case \(\hat{\beta}\) does not exist.

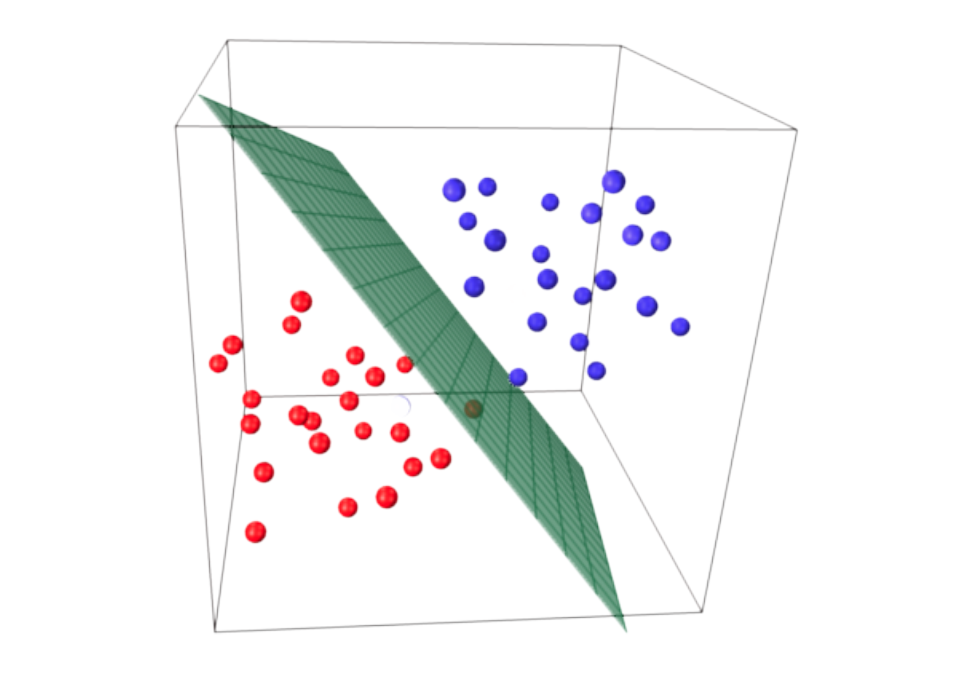

This occurs if there is non-overlap, i.e., separation by a hyperplane of the \(x_i\) for which \(y_i = 0\) and those for which \(y_i = 1\).

Non-Overlap Situation

Mathematically, there is non-overlap if there exists \(\alpha \in \mathbb{R}^p\) such that

\[\begin{cases} \text{for all } i \text{ such that } y_i = 0, & \alpha^T x_i \geq 0 \\ \text{for all } i \text{ such that } y_i = 1, & \alpha^T x_i \leq 0 \end{cases}\]

Illustration of Non-Overlap Situation

Non-Overlap and Existence

Proposition (admitted)

In case of non-overlap, the estimator \(\hat{\beta}\) does not exist, in the sense that \(L(\beta)\) is maximal when \(\|\beta\| \to \infty\) (in one or several directions).

For all \(x\), \(\hat{p}(x) \in \{0,1\}\), depending on the position of \(x\) relative to the separating hyperplane.

Nevertheless, there is a “dead zone” in the middle of the \(2\) point clouds, because the separating hyperplane is not necessarily unique.

Beyond the Dead Zone

Beyond this dead zone, classification is very simple (\(0\) or \(1\)).

But no interpretation of the model is possible (the OR are worth \(0\) or \(+\infty\)).

Existence and Uniqueness of MLE

We say there is overlap when no hyperplane can separate the red points from the blue points.

Proposition (admitted)

If \(\text{rank}(X) = p\) and there is overlap, then the MLE exists and is unique.

Under these conditions, we can therefore search for the MLE using the Newton-Raphson algorithm.

the maximum exists,

the function to optimize is strictly concave and there is therefore no local maximum, only a global maximum.

Fisher Information (Recall)

Let \(X\) be the design matrix (whose rows are the vectors \(x_i\)).

Let \(J_n(\beta)\) be the Fisher information matrix:

\[J_n(\beta) = -E\left[\frac{\partial^2 L}{\partial \beta^2}(\beta) \right]\]

Asymptotic Efficiency

Proposition (admitted)

In the logistic regression model, if

- the distribution of the regressors \((X_1, \ldots, X_p)\) has compact support,

- \(\text{rank}(X) = p\),

- the smallest eigenvalue of \(X^T X\) tends to infinity with \(n\),

then

the maximum likelihood estimator \(\hat{\beta}\) is consistent;

\(J_n(\beta)^{1/2}(\hat{\beta} - \beta) \xrightarrow{L} N(0, I_p)\)

where \(I_p\) is the identity matrix of size \(p\).

Comparison: Linear Regression

The formula for \(\hat{\beta}\) is explicit: \(\hat{\beta} = (X^T X)^{-1} X^T Y\);

Its expectation and variance are explicit;

In the Gaussian model (\(Y|X\) Gaussian), the distribution of \(\hat{\beta}\) is explicit, which allows constructing exact tests (Student, Fisher).

If the model is not Gaussian, these tests are valid asymptotically.

Comparison: Logistic Regression

No explicit formula for \(\hat{\beta}\), the solution is obtained numerically;

We know neither the bias nor the variance of \(\hat{\beta}\);

The distribution of \(Y|X\) is simple (a Bernoulli), but we don’t know the distribution of \(\hat{\beta}\).

We only know its asymptotic distribution.

We’ll do asymptotic tests!

Wald Tests and Confidence Intervals

Asymptotic Framework

Under “good conditions”,

\[J_n(\beta)^{1/2}(\hat{\beta} - \beta) \xrightarrow{L} N(0, I_p)\]

where \(J_n(\beta)\) is the Fisher information matrix.

To build asymptotic tests, we need to understand \(J_n(\beta)\) and be able to estimate it.

Computation of Jₙ(β)

\[J_n(\beta) = -E\left[\frac{\partial^2 L}{\partial \beta^2}(\beta) \bigg| X\right]\]

where \(L\) is the log-likelihood of the model.

From the proof of existence of MLE,

\[J_n(\beta) = \sum_{i=1}^n p_\beta(x_i)(1 - p_\beta(x_i)) x_i x_i^T\]

Equivalent Form

We can write equivalently

\[J_n(\beta) = X^T W_\beta X\]

where \(X\) is the design matrix and \(W_\beta\) is the diagonal matrix

\[W_\beta = \begin{pmatrix} p_\beta(x_1)(1 - p_\beta(x_1)) & 0 & \cdots & 0 \\ 0 & p_\beta(x_2)(1 - p_\beta(x_2)) & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & p_\beta(x_n)(1 - p_\beta(x_n)) \end{pmatrix}\]

Estimating the Information Matrix

To estimate \(J_n(\beta)\), we simply replace \(\beta\) by the MLE \(\hat{\beta}\)

Under the same regularity assumptions, we can show that

\[J_n(\hat{\beta})^{1/2}(\hat{\beta} - \beta) \xrightarrow{L} N(0, I_p)\]

Estimated Variance of β̂ⱼ

\[J_n(\hat{\beta})^{1/2}(\hat{\beta} - \beta) \xrightarrow{L} N(0, I_p)\]

Denoting \(\hat{\sigma}_j^2\) the \(j\)-th diagonal element of \(J_n(\hat{\beta})^{-1}\), we obtain (admitted):

\[\frac{\hat{\beta}_j - \beta_j}{\hat{\sigma}_j} \xrightarrow{L} N(0, 1)\]

Confidence Interval

We deduce a confidence interval for \(\beta_j\), at asymptotic confidence level \(1 - \alpha\):

\[\text{CI}_{1-\alpha}(\beta_j) = \left[\hat{\beta}_j - q_{1-\alpha/2}\hat{\sigma}_j \,;\, \hat{\beta}_j + q_{1-\alpha/2}\hat{\sigma}_j\right]\]

where \(q(1 - \alpha/2)\) is the quantile of order \(1 - \alpha/2\) of the \(N(0, 1)\) distribution.

We verify that we have \(\P(\beta_j \in \text{CI}_{1-\alpha}(\beta_j)) \to 1 - \alpha\).

Significance Test for One Coefficient

We want to test \(H_0: \beta_j = 0\) against \(H_1: \beta_j \neq 0\).

Under \(H_0\) we know that \(\frac{\hat{\beta}_j}{\hat{\sigma}_j} \xrightarrow{L} N(0, 1)\)

We deduce a critical region at asymptotic level \(\alpha\):

\[\mathcal R_\alpha = \left\{\frac{|\hat{\beta}_j|}{\hat{\sigma}_j} > q_{1-\alpha/2}\right\}\]

Indeed \(P_{H_0}(\mathcal R_\alpha) \to \alpha\).

This test is called the Wald test. (As any other test that relies on asymptotic normality)

P-value

Denoting \(\Phi\) the cdf of the \(\mathcal N(0, 1)\) distribution, the p-value of the test equals

\[p\text{-value} = 2\left(1 - \Phi\left(\frac{|\hat{\beta}_j|}{\hat{\sigma}_j}\right)\right)\]

Example in R

| Variable | Estimate | Std. Error | z value | Pr(> | z |

|---|---|---|---|---|---|

| (Intercept) | -3.9564361 | 0.3155529 | -12.538 | < 2e-16 | *** |

| AGE | 0.0640837 | 0.0123960 | 5.170 | 2.34e-07 | *** |

| I(AGE^2) | -0.0006758 | 0.0001260 | -5.364 | 8.14e-08 | *** |

| DBP | 0.0121546 | 0.0033775 | 3.599 | 0.00032 | *** |

| SEXEFEMME | 0.5155651 | 0.0776229 | 6.642 | 3.10e-11 | *** |

| WALK1 | -0.4042257 | 0.0913195 | -4.426 | 9.58e-06 | *** |

| ACTIV1 | -0.6573558 | 0.1150226 | -5.715 | 1.10e-08 | *** |

Each column corresponds resp. to

- \(\hat \beta_j\)

- \(\hat \sigma_j\)

- \(\hat \beta_j/\hat \sigma_j\) (z-score).

Estimation of an Odds-Ratio

We consider two individuals \(1\) and \(2\) who differ only by their regressor \(j\). Then,

\[OR(x_1^{(j)}, x_2^{(j)}) = e^{\beta_j(x_1^{(j)} - x_2^{(j)})}\]

Do we have \(OR(x_1^{(j)}, x_2^{(j)})\approx 1\)?

The estimation of \(OR(x_1^{(j)}, x_2^{(j)})\) is simply

\[\widehat{OR}(x_1^{(j)}, x_2^{(j)}) = e^{\hat{\beta}_j(x_1^{(j)} - x_2^{(j)})}\]

Important Example

If regressor \(j\) is binary with \(x_1^{(j)} = 1\) and \(x_2^{(j)} = 0\), then

\[\widehat{OR}(x_1^{(j)}, x_2^{(j)}) = e^{\hat{\beta}_j}\]

Asymptotic CI for an Odds-Ratio

We have seen that an asymptotic CI at confidence level \(1 - \alpha\) for \({\beta}_j\) is

\[\text{CI}_{1-\alpha}(\beta_j) = \left[\hat{\beta}_j - q_{1-\alpha/2}\hat{\sigma}_j \,;\, \hat{\beta}_j + q_{1-\alpha/2}\hat{\sigma}_j\right]= [l,r]\]

If \(x_1^{(j)} > x_2^{(j)}\), an asymptotic CI for \(OR(x_1^{(j)}, x_2^{(j)})= e^{\beta_j(x^{(j)}_1 - x^{(j)}_2)}\) at level \(1 - \alpha\) is

\[\text{CI}_{1-\alpha}(OR(x_1^{(j)}, x_2^{(j)})) = \left[e^{l(x_1^{(j)} - x_2^{(j)})}, e^{r(x_1^{(j)} - x_2^{(j)})}\right]\]

Significance Test for an Odds-Ratio

We generally want to compare \(OR(x_1^{(j)}, x_2^{(j)})\) to \(1\).

\[OR(x_1^{(j)}, x_2^{(j)}) = 1 \Leftrightarrow e^{\beta_j(x_1^{(j)} - x_2^{(j)})} = 1 \Leftrightarrow \beta_j = 0\]

Two-Sided Test

\(H_0: OR(x_1^{(j)}, x_2^{(j)}) = 1\) VS \(H_1: OR(x_1^{(j)}, x_2^{(j)}) \neq 1\)

amounts to testing \(H_0: \beta_j = 0\) against \(H_1: \beta_j \neq 0\). The Rejection region at level \(\alpha\) is

\[\mathcal R_\alpha = \left\{\frac{|\hat{\beta}_j|}{\hat{\sigma}_j} > q_{1-\alpha/2}\right\}\]

One-Sided Tests

Nevertheless, for ORs, we often prefer one-sided tests.

\(H_0: OR(x_1^{(j)}, x_2^{(j)}) = 1\) VS \(H_1: OR(x_1^{(j)}, x_2^{(j)}) > 1\)

If \(x_1^{(j)} > x_2^{(j)}\). Since \(OR(x_1^{(j)}, x_2^{(j)}) \geq 1 \Leftrightarrow \beta_j \geq 0\) rejection region at level \(\alpha\) is

\[\mathcal R_{\alpha}=\left\{\frac{\hat{\beta}_j}{\hat{\sigma}_j} > q_{1-\alpha}\right\}\]

Deviance

Saturated Model

Suppose we have \(n\) observations \((Y_1, \dots, Y_n)\) and \((X_1, \dots, X_n)\) (categorical)

Here \(X_k\) can represent the vector \(X_k = (X^{(1)}_k, \dots, X^{(p)}_k)^T\).

Assume that individuals are iid, with \(\mathbb P(Y=1|X_k=x) = p(x)\).

How do we estimate \(p(x)\)?

Saturated Estimator

Suppose we have \(n\) observations \((Y_1, \dots, Y_n)\) and \((X_1, \dots, X_n)\)

\(n(x) = |\{k:~ X_k = x\}|\) (number of indiv. \(k\) s.t. \(X_k=x\))

\(n_1(x) = |\{k:~ X_k = x ~~\text{and}~~Y_k=1\}|\)

The saturated model is one that estimates \(p(x)\), for an observed \(x\), by

\[\hat{p}_{\text{sat}}(x) = \frac{n_1(x)}{n(x)}\]

Remark: Distinct Observations

\[\hat{p}_{\text{sat}}(x) = \frac{n_1(x)}{n(x)}\]

If all observations are distinct, i.e., each observed \(x\) is only for a single individual, then for an observed \(x\):

\(n(x) = 1\), \(n_1(x) \in \{0,1\}\), and \(\hat{p}_{\text{sat}}(x) = 0\) or \(1\).

Properties of the Saturated Model

The saturated model is the simplest model to imagine.

It fits the data perfectly.

However, it has no explanatory power (effect of regressors on \(Y\)?).

And it says nothing about \(p(x)\) if \(x\) is not observed.

It will serves as a reference for fit

Likelihood of Saturated Estimator

For the saturated model with probabilities \(p(x)\), the Log-likelihood is:

\[L(y_1, \ldots, y_n|x_1, \ldots, x_n) = \sum_{i=1}^n y_i \ln(p(x_i)) + (1 - y_i) \ln(1 - p(x_i))\]

The saturated model maximizes this likelihood, and we denote

\[L_{\text{sat}} = \sum_{i=1}^n y_i \ln(\hat p_{\text{sat}}(x_i)) + (1 - y_i) \ln(1 - \hat p_{\text{sat}}(x_i))\]

Case 1: Distinct Observations

If all observations \(x_i\) are distinct, we have \(\hat{p}_{\text{sat}}(x_i) = y_i\) with \(y_i \in \{0, 1\}\). We thus have

\[L_{\text{sat}} = 0\]

The saturated estimator has highest possible log-likelihood: it fits the data perfectly (too well).

Case 2: Non-Distinct Observations

If the observations \(x_i\) are not distinct, we obtain

\[L_{\text{sat}} = \sum_x \left[n_1(x) \ln\left(\frac{n_1(x)}{n(x)}\right) + (n(x) - n_1(x)) \ln\left(1 - \frac{n_1(x)}{n(x)}\right)\right]\]

where the sum runs over the set of values \(x\) taken by the \(x_i\).

Deviance

The deviance of a model measures how much this model deviates from the saturated model (the ideal model in terms of likelihood).

\[D = 2(L_{\text{sat}} - L_{\text{mod}})\]

where \(L_{\text{mod}}\) denotes the log-likelihood for the model parameters.

We always have \(D \geq 0\).

If all observations are distinct, \(L_{\text{sat}} = 0\) therefore \(D = -2L_{\text{mod}}\)

Role of Deviance and Computation in R

\[D = 2(L_{\text{sat}} - L_{\text{mod}})\]

Deviance plays the role of the SSR of a linear model: the higher the deviance, the less well the model is fitted to the data.

In R, The returned deviance is \(-2L_{\text{mod}}\): the term \(L_{\text{sat}}\) is therefore omitted.

Deviance Tests and Model Selection

Linear Constraint Test

As in linear regression, we would like to test \(H_0: R\beta = 0\) VS \(H_1: R\beta \neq 0\)

where \(R\) is a constraint matrix of size \((q, p)\) of full rank.

For recall, depending on the choice of \(R\) this allows:

testing the minimum: is there at least one relevant regressor?

comparing nested models

examining the collective significance of a family of regressors

Available Procedures

In GLM, several test procedures address the problem.

The Wald test, based on the asymptotic normality of \(\hat{\beta}\), which generalizes the one seen for testing \(\beta_j = 0\) against \(\beta_j \neq 0\).

The likelihood ratio test, called in this context the deviance test.

The score test, based on the behavior of the gradient of the log-likelihood at the critical point.

The most used is the deviance test.

The Deviance Test (or Likelihood Ratio Test)

To test \(H_0: R\beta = 0\) against \(H_1: R\beta \neq 0\), the principle of the test is as follows:

We calculate the MLE in each model to obtain \(\hat{\beta}\) in the complete model and \(\hat{\beta}_{H_0}\) in the constrained model.

Logic: If \(H_0\) is true, the constrained model should be as “likely” as the complete model, so \(L(\hat{\beta})\) and \(L(\hat{\beta}_{H_0})\) should be similar.

Deviance Test Statistic

The test statistic is the difference of deviances:

\[D_{H_0} - D_{H_1} = 2\left(L(\hat{\beta}) - L(\hat{\beta}_{H_0})\right)\]

Under \(H_0\), denoting \(q\) the number of constraints, we have the convergence (admitted):

\[D_{H_0} - D_{H_1} = 2\left(L(\hat{\beta}) - L(\hat{\beta}_{H_0})\right) \xrightarrow{L} \chi^2_q\]

Rejection Region and P-value

The asymp. rejection region at asymptotic level \(\alpha\) is therefore

\[\mathcal R_\alpha = \{D_{H_0} - D_{H_1} > \chi^2_{q,1-\alpha}\}\]

where \(\chi^2_{q,1-\alpha}\): quantile \(1 - \alpha\) of a \(\chi^2_q\) distribution.

The p-value equals

\[p\text{-value} = 1 - F(D_{H_0} - D_{H_1})\]

where \(F\) is the cdf of a \(\chi^2_q\) distribution.

Special Case 1: Significance Test

We want to test if a model (having a constant) is significant

We therefore test \(H_0\): all its coefficients are zero except the constant. This corresponds to the special case

\(R = [0 | I_{p-1}]\).

We compare the deviance of the model to the null deviance \(D_0\), corresponding to a model that contains only the constant.

Test Statistic

The test statistic is \(D_0 - D\). Under \(H_0\), when \(n \to \infty\):

\[D_0 - D \sim \chi^2_{p-1}\]

The model is therefore significant (relative to the null model) if the sample is in the critical region of asymptotic level \(\alpha\):

\[\mathcal R_\alpha = \{D_0 - D > \chi^2_{p-1,1-\alpha}\}\]

Special Case 2: Nested Models

Suppose that model \(1\) (with deviance \(D_1\)) is a sub-model of model \(2\) (with deviance \(D_2\))

Model \(1\) is therefore obtained from model \(2\), with parameter \(\beta\), via a constraint of the type \(R\beta = 0\) where \(R\) is a \((q, p)\) matrix.

Under \(H_0: R\beta = 0\), we have asymptotically \(D_1 - D_2 \sim \chi^2_q\)

Hence the asymptotic test:

\(\mathcal R_\alpha = \{D_1 - D_2 > \chi^2_{q,1 - \alpha}\}\)

AIC and BIC Criteria

The AIC and BIC criteria are defined similarly to linear regression, i.e.

\(\text{AIC} = -2L_{\text{mod}} + 2p\)

\(\text{BIC} = -2L_{\text{mod}} + \ln(n)p\)

where \(L_{\text{mod}}\) is the log-likelihood of the estimated model.

AIC and BIC via Deviance

If we ignore saturated likelihood and set \(L_{\text{sat}}=0\),

\(\text{AIC} = D + 2p\)

\(\text{BIC} = D + \ln(n)p\)

In practice, we choose the model having the minimal AIC or BIC

As in linear regression, we can use automatic selection procedures (backward, forward, etc).

Example: Obesity Study

| Statistic | Value | Degrees of Freedom |

|---|---|---|

| Null deviance | \(4610.8\) | on \(5300\) |

| Residual deviance | \(4459.5\) | on \(5290\) |

| AIC | \(4481.5\) |

The model deviance is therefore \(D = 4459.5\).

Significance Test: We compare \(D\) to the null deviance \(D_0 = 4610.8\): \(D_0 - D = 151.3\). The p-value of the test equals \(1 - \chi^2_{10}(151.3) \approx 0\) where \(\chi^2_{10}\) is the cdf of a \(\chi^2_{10}\).

The model is significant.

Example: Significance Test of MARITAL

| Statistic | Value | Degrees of Freedom |

|---|---|---|

| Null deviance | \(4610.8\) | on \(5300\) |

| Residual deviance | \(4462.7\) | on \(5295\) |

| AIC | \(4474.7\) |

The deviance is now \(D_2 = 4462.7\). To compare with the previous model, we calculate: \(D_2 - D = 3.2\).

The p-value of the test equals \(1 - F_5(3.2) \approx 0.67\), where \(F_5\): cdf of a \(\chi^2_5\).

We therefore accept \(H_0\): the coefficients related to MARITAL are zero. (Also confirmed with AIC)

Example: Significance Test of AGE²

| Statistic | Value | Degrees of Freedom |

|---|---|---|

| Null deviance | \(4610.8\) | on \(5300\) |

| Residual deviance | \(4439.5\) | on \(5294\) |

| AIC | \(4453.5\) |

The deviance test with the previous model has p-value \(1 - F_1(4462.7 - 4439.5) = 1 - F_1(23.2) \approx 10^{-6}\)

This model is therefore preferable, (confirmed with AIC).

However, we cannot compare this model with the first one by deviance test because they are not nested.

We can however compare their AIC: this model is preferable.

Prediction

Setting and Objective

Suppose we are interested in a new individual for whom

- we know their characteristics \(x \in \mathbb{R}^p\),

- we do not know their \(Y\).

We want to predict \(Y\) for this new individual.

Recall in the Logit Model

If we have fitted a logistic regression model, we can estimate

\[p_\beta(x) = P(Y = 1|X = x)\]

by

\[p_{\hat{\beta}}(x) = \text{logit}^{-1}(x^T \hat{\beta}) = \frac{e^{x^T \hat{\beta}}}{1 + e^{x^T \hat{\beta}}}\]

Outline for Prediction

\[p_\beta(x) = P(Y = 1|X = x)\]

We will see:

how to construct a confidence interval around the estimation \(p_{\hat{\beta}}(x)\);

how to exploit this estimation to classify the new individual in category \(Y = 0\) or \(Y = 1\).

CI: Asymptotic Distribution of p_β(x)

We know that when \(n \to \infty\):

\[\hat{\beta} \sim N(\beta, (X^T W_{\hat{\beta}} X)^{-1})\]

- \(X=(X^{(1)}, \dots, X^{(p)})\) is the \(n \times p\) design matrix

- \(W_{\hat{\beta}}\) is the \(n \times n\) diagonal matrix with coefs \(p_{\hat \beta}(x_i)(1-p_{\hat \beta}(x_i))\)

CI for Linear Predictor

We deduce that when \(n \to +\infty\), \(x^T \hat{\beta} \sim N(x^T \beta, x^T (X^T W_{\hat{\beta}} X)^{-1} x)\), and the asymptotic CI of \(x^T\beta\):

\[\text{CI}_{1-\alpha}(x^T \beta) = \left[x^T \hat{\beta} \pm q_{1-\alpha/2} \sqrt{x^T (X^T W_{\hat{\beta}} X)^{-1} x}\right]\]

CI for Probability pβ(x)

Since \(p_{\hat{\beta}}(x) = \text{logit}^{-1}(x^T \hat{\beta})\), we have therefore by application of the increasing function \(\text{logit}^{-1}\), the CI at asymptotic level \(1 - \alpha\):

\[\text{CI}_{1-\alpha}(p_\beta(x)) = \left[\text{logit}^{-1}\left(x^T \hat{\beta} \pm q_{1-\alpha/2} \sqrt{x^T (X^T W_{\hat{\beta}} X)^{-1} x}\right)\right]\]

Classification

We have estimated \(p_\beta(x) = P(Y = 1|X = x)\) by \(p_{\hat{\beta}}(x)\).

For a threshold to choose \(s \in [0, 1]\), we use the rule:

\[\begin{cases} \text{if } p_{\hat{\beta}}(x) > s, & \hat{Y} = 1 \\ \text{if } p_{\hat{\beta}}(x) < s, & \hat{Y} = 0 \end{cases}\]

The “natural” choice of threshold is \(s = 0.5\) but this choice can be optimized.

Confusion Matrix

We proceed by cross-validation:

Using a train sample, predict \(Y\) on a test sample and form the confusion matrix.

| \(Y = 0\) | \(Y = 1\) | |

|---|---|---|

| \(\hat{Y} = 0\) | TN | FN |

| \(\hat{Y} = 1\) | FP | TP |

Reading: T: true, F:False, N: Negative, P: Positive.

FP: false positives: number of individuals who were classified positive who were actually negative

Sensitivity and Specificity

The ideal is to have a confusion matrix that is as diagonal as possible.

We generally seek to maximize the following indicators:

The sensitivity (or recall, or true positive rate) estimates \(\P(\hat{Y} = 1|Y = 1)\) by

\[\frac{\text{TP}}{\text{TP} + \text{FN}}\]

The specificity (or selectivity, or true negative rate) estimates \(\P(\hat{Y} = 0|Y = 0)\)

\[\frac{\text{TN}}{\text{TN} + \text{FP}}\]

Other Indicators

The precision (or positive predictive value) estimates \(\P(Y = 1|\hat{Y} = 1)\) by

\(\frac{\text{TP}}{\text{TP} + \text{FP}}\)

The \(F\)-score is the harmonic mean between sensitivity and precision:

\[F_1 = 2 \frac{\text{precision} \times \text{sensitivity}}{\text{precision} + \text{sensitivity}}\]

Choice of Threshold s

For each threshold \(s\), from a test sample:

- we can form the confusion matrix

- calculate scores (sensitivity, \(F\)-score, etc.)

We finally choose the optimal threshold \(s\), according to the chosen score.

Choosing the score

- It depends on the context of the study

- It can be much more serious to wrongly predict \(\hat{Y} = 0\) than \(\hat{Y} = 1\)

\(\hat Y=1\) (treatment) while the patient is not ill (\(Y = 0\))

\(\hat Y=0\) (no treatment) while the patient has a serious illness (\(Y=1\))

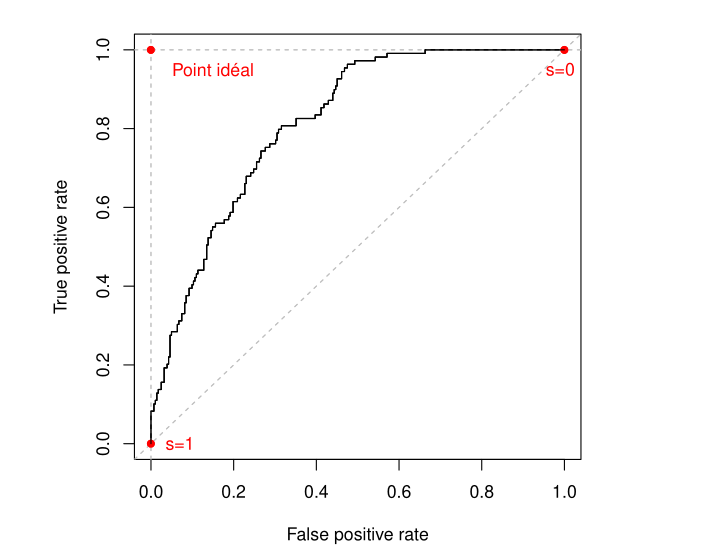

ROC Curve

We can also plot the ROC curve (TP rate as a function of FP rate for \(s \in [0, 1]\)):

\(ROC:~~\mathrm{sensitiv.} = \frac{TP}{TP+FN} = F\left(\frac{FP}{FP+TN}\right) = F(1-\mathrm{specific.})\)

The AUC (area under the curve) is a quality indicator of the model (\(0 \leq \text{AUC} \leq 1\)).

Or equivalently, the Gini index: \(2 \times \text{AUC} - 1\).

Use: compare \(2\) models by plotting the 2 ROC curves.

ROC Curve Illustration

Comments

Under these conditions, the MLE therefore exists for sufficiently large \(n\). In fact, there is necessarily overlap when \(n\) is large.

It is asymptotically efficient (= minimal asymptotic variance)

The Fisher information matrix \(J_n(\beta)\) can be calculated

We will be able to rely on asymptotic normality to perform tests and construct confidence intervals